Introduction

Portfolio optimization involves selecting asset allocations to balance expected returns and risk. As the number of decision factors and data sources increases, incorporating non-standard predictors into the optimization process becomes challenging. This article presents a framework for applying deep reinforcement learning to address these challenges.

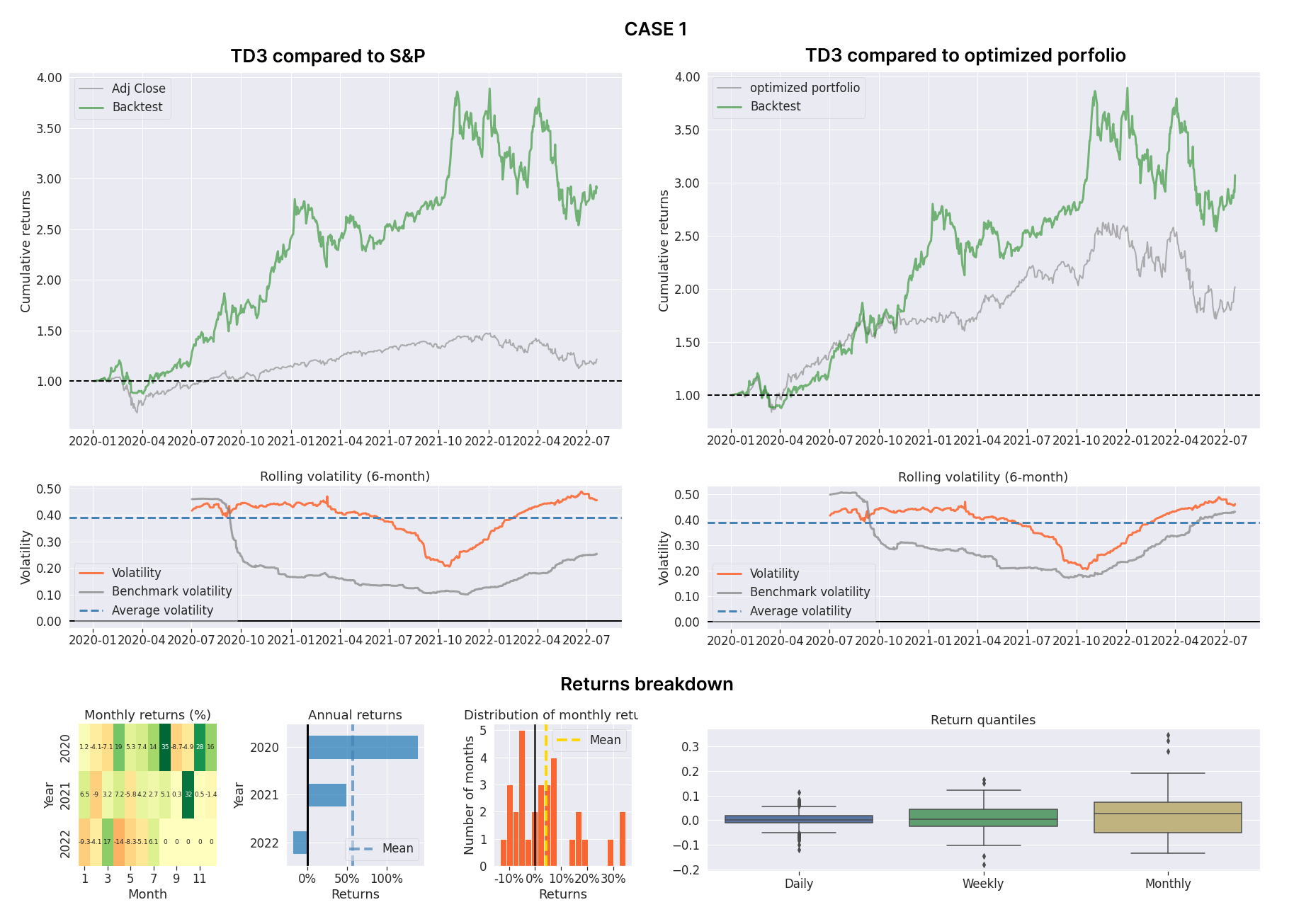

RL portfolio optimization results example

RL portfolio optimization results example

Publication and Citation

Publication: Analytics in Finance and Risk Management, Chapter 7

Publisher: CRC Press, Taylor & Francis Group

Year: 2023

Author: Filip Wójcik

Pages: 31

Access: View Chapter

Citation: Wójcik, F. (2023). A Deep Reinforcement Learning Approach for Portfolio Optimization and Risk Management – Case Studies. In Analytics in Finance and Risk Management (1st ed., Chapter 7, pp. 31). CRC Press. https://doi.org/10.1201/9780367854690-7

Publication Overview

This work introduces deep reinforcement learning methodologies for portfolio optimization and evaluates their performance in volatile and stochastic market environments. The research comprises a literature review of selected portfolio optimization techniques using deep reinforcement learning algorithms, followed by experimental validation in challenging market conditions.

Traditional Portfolio Optimization Limitations

Many portfolio optimization techniques are based on different variants of constrained quadratic programming formalizations. These traditional methods take as inputs expected asset returns, forms of risk metrics such as covariance matrices, and transaction costs. The goal is typically selected as either maximization of return while keeping the risk level constant or minimizing the risk with varying returns. The problem is then solved either via a closed-form equation or a gradient-minimizing approach.

These approaches face limitations when incorporating the increasing variety of non-standard predictors and decision factors available in modern financial markets.

Deep Reinforcement Learning Framework

Prior studies on deep reinforcement learning show that this family of algorithms can achieve strong performance in complex, volatile, and stochastic environments. Deep reinforcement learning extends classic reinforcement learning approaches that utilize tabular calculation or function approximation methods.

Portfolio optimization can be perceived as a multi-stage decision problem, which aligns with the strengths of deep reinforcement learning for sequential decision making.

Research Structure

The research is organized into two components. The first part presents a literature review of selected portfolio optimization techniques that use deep reinforcement learning algorithms. This review establishes the theoretical foundation and examines existing approaches in the field.

The second part presents experiments conducted on stock simulators and different assets in challenging market conditions after the COVID-19 outbreak and subsequent events. These experiments provide empirical validation of the approaches under stress conditions.

Experimental Methodology

The experimental framework evaluates deep reinforcement learning agents against benchmarks, including stock market indices and classic optimization strategies. The evaluation employs multiple performance metrics to ensure comprehensive assessment of the approaches.

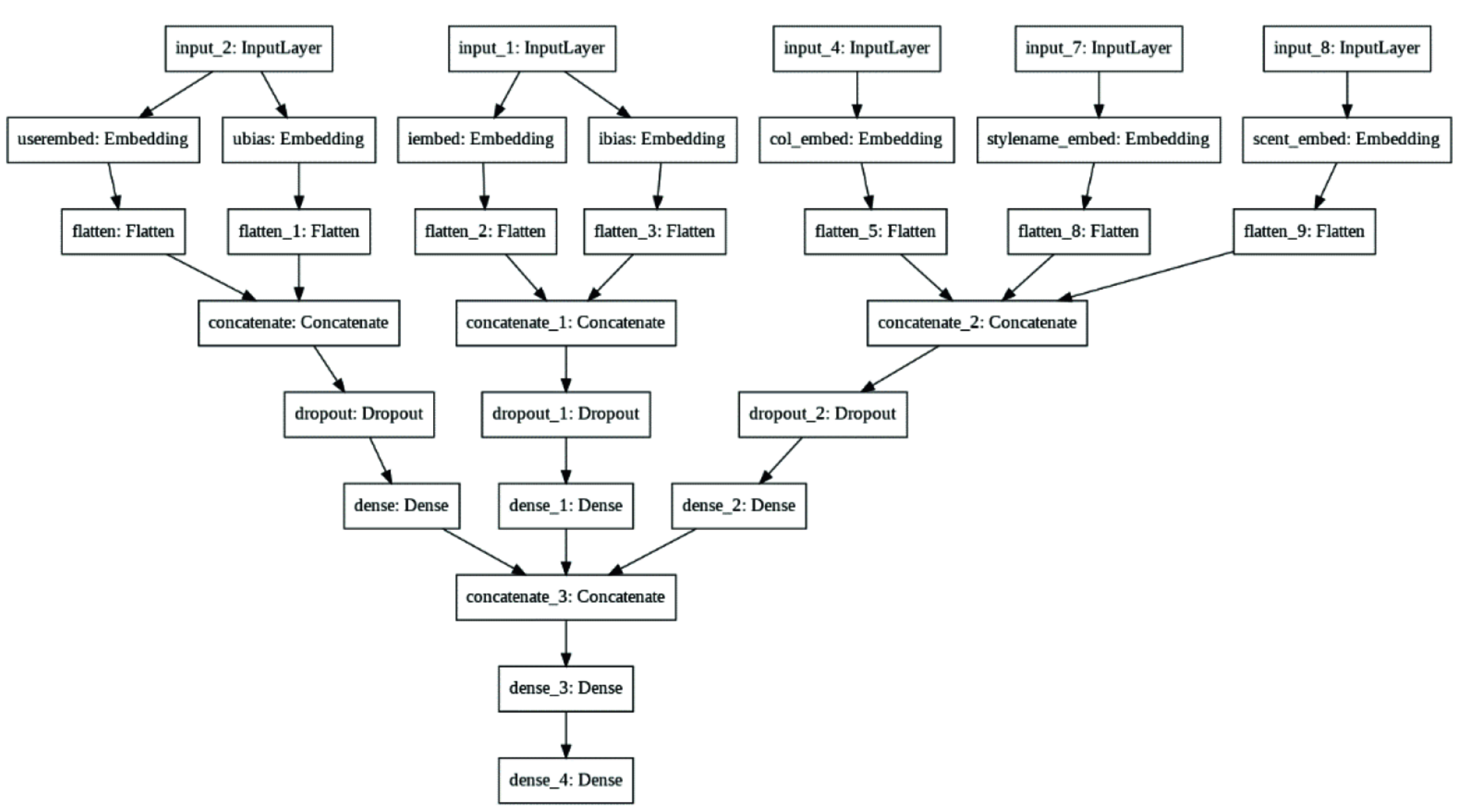

The deep reinforcement learning agents take as input multiple non-standard factors, including several technical indicators and summary statistics, extending beyond a typical quadratic programming setting. This expanded input space allows the agents to leverage information that traditional methods cannot effectively incorporate.

The comparison between deep reinforcement learning agents and benchmarks uses four performance metrics.

- The Sharpe ratio measures risk-adjusted returns.

- The Calmar ratio evaluates the relationship between returns and maximum drawdown.

- Cumulative returns indicate overall performance over the evaluation period.

- Annual volatility quantifies the risk level of the strategies.

Experimental Results

The evaluated deep reinforcement learning algorithms outperformed benchmarks in terms of cumulative returns and Sharpe ratio in the studied setups, including post-COVID-19 market conditions.

These results suggest adaptability and robustness compared to traditional optimization methods, particularly when processing non-standard factors and changing market regimes.

Validation in Crisis Conditions

The experiments specifically considered market conditions after the COVID-19 outbreak and subsequent events. Performance during these periods illustrates practical applicability for portfolio management.

Theoretical Significance

The experimental results support the use of deep reinforcement learning for complex, stochastic, multi-stage decision problems that include additional information sources. This supports deep reinforcement learning as a complementary alternative to traditional portfolio optimization methods, particularly for high-dimensional input spaces and non-linear relationships.

Future Research Directions

Further research is needed to improve reproducibility, variance reduction, and interpretability. These areas are critical for broader adoption of deep reinforcement learning in portfolio management.

Reproducibility concerns arise from the stochastic nature of financial markets and the training process of deep reinforcement learning agents. Establishing protocols for consistent performance across different initializations and market conditions remains an important objective.

Variance reduction in deep reinforcement learning outputs is essential for practical implementation, as excessive variability in portfolio decisions can lead to increased transaction costs and reduced investor confidence. Developing techniques to stabilize agent behavior while maintaining adaptability remains a challenge.

Interpretability of deep reinforcement learning decisions is crucial for regulatory compliance and investor trust. Understanding why agents make specific portfolio allocation decisions and explaining these choices to stakeholders is important for institutional adoption.

Practical Implications

The research indicates that deep reinforcement learning can handle the increasing complexity of portfolio optimization problems. By incorporating non-standard predictors and adapting to dynamic market conditions, these approaches offer advantages over traditional quadratic programming methods.

The ability to process multiple technical indicators and summary statistics simultaneously allows deep reinforcement learning agents to identify patterns and relationships that conventional methods might miss. This capability is valuable in markets characterized by increasing interconnectedness and information flow.

Conclusion

This research evaluates deep reinforcement learning as an approach to portfolio optimization in complex, volatile market environments. Experimental validation during post-COVID-19 market conditions demonstrates practical applicability in the studied setups. Further work on reproducibility, variance reduction, and interpretability is recommended.